Changes in the taxes for self-employed persons effective from 2025.

Here's everything you need to know!

With each passing year, the tax system adapts, responding to shifts in tax laws or fluctuations in economic indicators affecting mandatory tax contributions. What significant adjustments will self-employed individuals need to deal with in the upcoming year?

Flat-rate tax

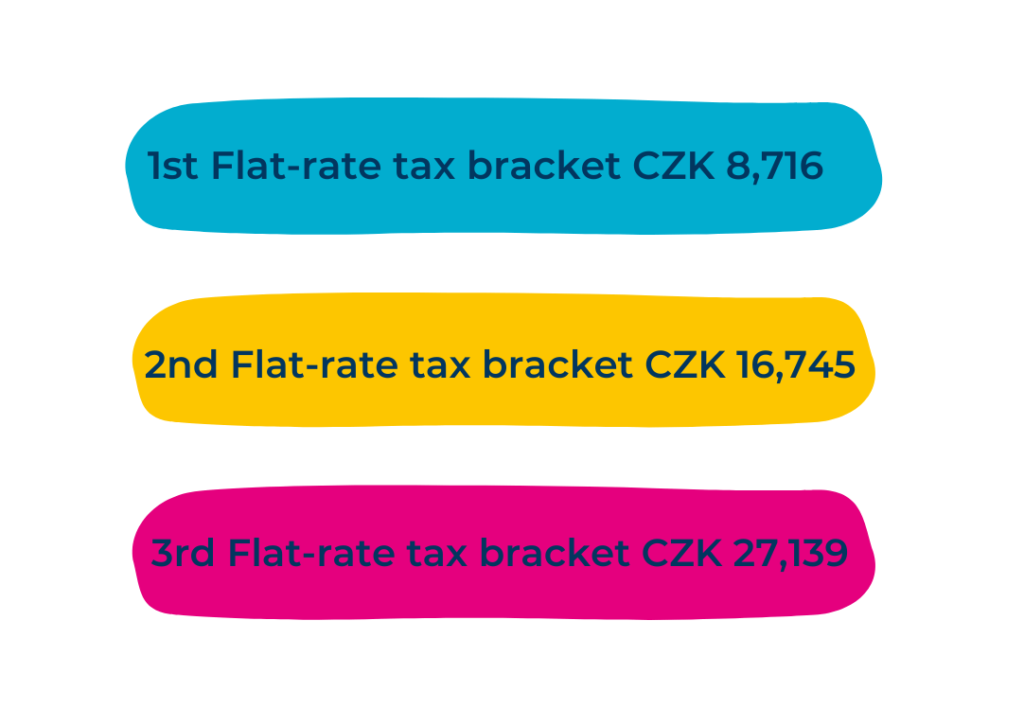

For self-employed professionals, the flat-rate tax offers a simplified taxation option. Meeting the specified conditions allows entrepreneurs to bypass the need for tax return submissions or social and health insurance reports. Instead, a consolidated monthly payment covers taxes, social security, and health insurance. As of 2025, this monthly sum is set as follows: Self-employed persons have the option to select the flat-rate tax bracket, but this choice is contingent upon meeting specific criteria associated with each bracket. These criteria typically encompass both the income level and the nature of the work undertaken by the individual.

Self-employed persons have the option to select the flat-rate tax bracket, but this choice is contingent upon meeting specific criteria associated with each bracket. These criteria typically encompass both the income level and the nature of the work undertaken by the individual.

Advance payments for the health and social insurance.

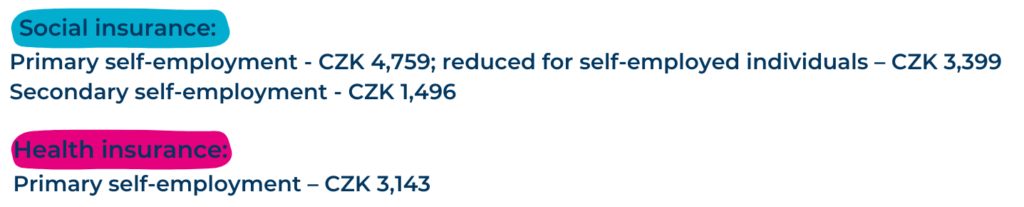

In general, the insurance premium amount is established as a percentage of the For self-employed individuals, the assessment base for insurance premiums will be 50% of the tax base, for social insurance purposes, it will already be 55% of the tax base. Nevertheless, it’s crucial to ensure that insurance premiums calculated using this method do not dip below the mandatory minimum premium. The minimum monthly advance payments for insurance premiums in 2025 are detailed as follows:

Mandatory minimum health insurance contributions do not apply to certain self-employed individuals. This category includes pensioners and students, for whom the state takes on the responsibility of covering insurance premiums. Additionally, self-employed individuals engaged in concurrent employment, where employment serves as their primary source of income, are also exempted.

Tax rate

The income tax rates of natural persons are 15% and 23%. From 2024, there is a change in the tax base to which each rate applies.

- The part of the tax base up to 36 times the average wage is subject to a 15% tax rate.

- The part of the tax base exceeding 36 times the average wage is subject to a 23% tax rate.

In 2024, 36 times the average wage is CZK 1 676 052.

Tax credit & deductions

Taxpayers are entitled to claim tax deductions and tax credits on their tax return (subject to conditions, although the scope of these is limited compared to previous years. A deductible item is the amount by which the tax base can be reduced, a tax credit is the crown-for-crown amount by which the tax itself can be reduced. In 2025, the following can be used:

Tax credits:

- Basic Taxpayer Credit

- Spousal discount

- Disability

- Disability card holders (ZTP/P)

- Child tax discount

Deductibles:

- Charitable donations

- Interests on housing loans

- Supplementary private and life insurance

People NOT considered Czech tax residents may reduce their tax base and their tax by the above deductibles and credits, ONLY if they are considered EU or EEA tax residents and if the final sum of their income from sources within the Czech Republic amounts to at least 90% of their total income. This does not apply to the basic taxpayer credit.

In summary, the primary deadline for submitting personal income tax returns for 2024 is 2nd April 2025. If the return is electronically filed, such as through a data mailbox, the deadline extends to 2 May 2025. If a tax adviser is authorized to file the return, the deadline is further extended to 1st July 2025. These same deadlines are applicable to the due date of the 2024 tax liability.

Furthermore, the deadlines for filing social security and health insurance statements for self-employed individuals are contingent on the tax return deadline, requiring submission within 1 month of the expected date for filing the income tax return.

Contacts: